The financial landscape is undergoing a dramatic transformation, fueled by the rise of Open Banking. This innovative approach to financial data sharing is empowering consumers and businesses alike, fostering greater competition, and driving the development of new and improved financial products and services. Open Banking, through secure and regulated Application Programming Interfaces (APIs), allows third-party providers access to consumer banking data, with the customer’s explicit consent. This access unlocks a wealth of possibilities, from personalized financial management tools and streamlined lending processes to innovative payment solutions and enhanced fraud detection capabilities. The implications of this shift are far-reaching and are reshaping the very foundation of the financial ecosystem.

This article will explore the multifaceted impact of Open Banking, examining its core principles, exploring its benefits for both consumers and businesses, and analyzing its role in driving innovation within the financial sector. We will delve into the key regulatory frameworks governing Open Banking, highlighting the importance of data security and privacy. Furthermore, we will discuss the future trajectory of Open Banking, considering its potential to revolutionize the way we interact with our finances and reshape the financial ecosystem as a whole. Understanding Open Banking is crucial for anyone navigating the modern financial landscape, from individual consumers to established financial institutions and aspiring fintech startups.

Definition of Open Banking

Open banking is a financial services term describing a system that securely shares financial data electronically with third-party providers. This sharing is facilitated through the use of application programming interfaces (APIs).

Essentially, open banking allows third-party developers to build applications and services that can access your financial data, with your explicit consent. This data can include everything from transaction history and balances to account details and regular payments.

The aim of open banking is to promote competition and innovation within the financial services industry, ultimately benefiting consumers with tailored products and services.

Customer Consent and Control

At the heart of open banking lies the principle of customer consent. Individuals retain complete control over their financial data and explicitly authorize which third-party providers can access it. This empowerment shifts the balance of power, placing consumers firmly in the driver’s seat.

Consent is granular and revocable. Customers can choose precisely which data is shared, with which providers, and for what purpose. They can also withdraw their consent at any time, effectively cutting off access to their information.

Third-Party Data Access Explained

At the heart of open banking lies the concept of third-party data access. This refers to the ability of authorized providers, beyond traditional financial institutions, to access consumer banking data through secure APIs (Application Programming Interfaces).

This access is granted with the explicit consent of the consumer. Consumers retain control over which data is shared, with which providers, and for what purpose. This framework empowers consumers to leverage their own financial data to access innovative financial products and services.

Examples of third-party data access include allowing a budgeting app to view transaction history or enabling a loan comparison website to assess creditworthiness. This data sharing facilitates more personalized and competitive financial offerings.

Use Cases: Aggregators and Smart Budgeting

Open banking significantly empowers aggregator platforms and smart budgeting applications. These services leverage API access to consolidate a user’s financial data from multiple institutions into a single dashboard. This provides a holistic view of their finances, enabling more informed decision-making.

Smart budgeting tools can automatically categorize transactions, track spending habits, and even provide personalized financial advice based on the aggregated data. This level of insight allows users to better manage their finances, identify areas for savings, and achieve their financial goals more effectively.

Improved Loan and Credit Products

Open banking has significantly impacted loan and credit products, primarily by enabling more accurate risk assessments. Lenders can access a broader view of an applicant’s financial history, including transaction data, spending habits, and other relevant information not typically available through traditional credit reports.

This access translates into faster loan approvals and the potential for more competitive interest rates. By leveraging open banking data, lenders can better understand an individual’s financial stability and offer personalized loan products tailored to their specific needs and risk profiles.

Furthermore, this enriched data allows lenders to extend credit to individuals who might have been previously excluded due to limited credit history or reliance solely on traditional credit scoring models.

Security and Privacy Measures

Security and privacy are paramount in open banking. Robust measures are essential to protect sensitive financial data.

Data encryption, multi-factor authentication, and secure APIs are fundamental components of a secure open banking ecosystem. These technologies help safeguard user data from unauthorized access and fraudulent activities.

Regulatory frameworks, such as PSD2 in Europe and the Consumer Financial Protection Bureau (CFPB) guidelines in the US, play a vital role in establishing security standards and ensuring consumer protection.

User consent is another crucial aspect. Individuals must explicitly authorize third-party providers to access their financial information. This ensures transparency and control over data sharing.

Regulations Around the World (PSD2, CDR)

Open Banking’s rise is fueled by regulations designed to foster competition and innovation in financial services. A prime example is the European Union’s Revised Payment Services Directive (PSD2), which mandates banks to open up customer data to third-party providers through secure APIs. This has catalyzed the growth of account aggregation, payment initiation, and other innovative services across Europe.

Beyond Europe, similar frameworks are emerging. Consumer Data Right (CDR) legislation, inspired by PSD2, is gaining traction in countries like Australia and the United Kingdom. These regulations aim to empower consumers with greater control over their financial data, enabling them to share it securely with accredited third-party providers for tailored financial products and services.

Collaboration Between Banks and Fintechs

Open banking has fostered a new era of collaboration between traditional banks and fintech companies. Rather than viewing each other solely as competitors, many institutions are recognizing the mutual benefits of partnerships.

Fintechs bring innovation, agility, and customer-centric design to the table. Banks offer established infrastructure, regulatory expertise, and a large customer base. By leveraging each other’s strengths, both parties can enhance their offerings and reach new markets.

This collaboration often takes the form of APIs, allowing fintechs to access customer data (with consent) and integrate their services with existing banking platforms. This results in a more seamless and personalized financial experience for consumers.

Benefits for Consumers and Businesses

Open banking offers numerous advantages for both consumers and businesses. For consumers, it promotes increased competition among financial providers, leading to better products and services. Personalized financial management tools become more accessible, empowering users to make informed decisions about their money. Streamlined account switching is another key benefit, making it easier for consumers to move to providers offering superior terms.

Businesses also stand to gain. Open banking enables the creation of innovative financial products tailored to specific business needs. Improved efficiency in areas like lending and payments processing reduces operational costs. Accessing richer financial data allows businesses to offer more competitive pricing and personalized services to their customers.

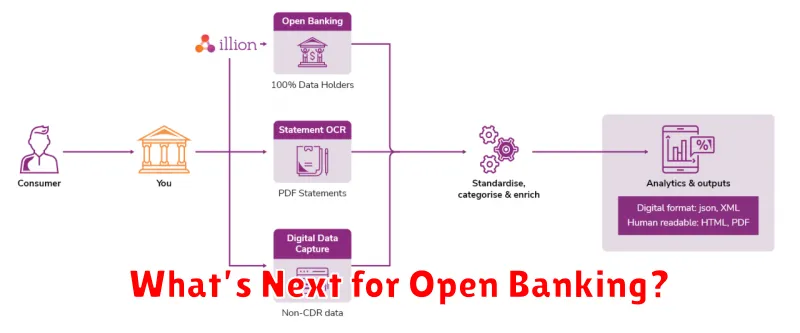

What’s Next for Open Banking?

Open banking is still evolving, and its future trajectory hinges on several key factors. Increased consumer adoption is crucial for widespread impact. This relies on building trust and demonstrating the tangible benefits of data sharing.

Standardization and interoperability are essential for seamless data exchange across different platforms and jurisdictions. Further development of APIs and common data formats will facilitate this.

Enhanced security measures are paramount to maintaining consumer confidence. Robust safeguards against fraud and data breaches are vital for the continued growth of open banking.

Beyond these core elements, the future of open banking likely involves expansion into new areas. This includes deeper integration with other sectors, like healthcare and telecommunications, offering personalized financial management tools, and facilitating more sophisticated lending and investment products.

{kind=link}