In today’s rapidly evolving financial landscape, the lines between traditional banking and digital finance are blurring. Consumers are increasingly presented with innovative options like digital wallets and digital banks, often leaving them wondering about the key distinctions. Understanding the difference between a digital wallet and a digital bank is crucial for making informed decisions about managing finances effectively and securely in the digital age. This article will delve into the core functionalities, benefits, and drawbacks of both digital wallets and digital banks to provide clarity on their respective roles in modern finance. We’ll explore how each platform addresses different financial needs and examine the security considerations associated with each.

While both digital wallets and digital banks operate within the digital realm, they offer distinct services and cater to different financial requirements. Digital wallets primarily focus on facilitating convenient and secure transactions, whereas digital banks offer a broader range of financial services, often mirroring traditional banks but without physical branches. By examining the fundamental differences between these two digital finance platforms, we can empower consumers to make strategic choices that align with their individual financial goals and priorities. This comparison will explore aspects like account management, transaction capabilities, fees, security measures, and regulatory oversight to provide a comprehensive overview of the digital wallet vs. digital bank debate.

Definitions and Core Functions

Understanding the difference between digital wallets and digital banks starts with defining each. A digital wallet is an electronic device, online service, or software program that allows one party to make electronic transactions with another. These transactions can be for a variety of goods or services and typically use near-field communication (NFC) technology.

In contrast, a digital bank is a financial institution that operates primarily online. It offers most of the same services as traditional banks, such as checking and savings accounts, loans, and money transfers, but without physical branches. Digital banks often leverage technology to provide more efficient and cost-effective services.

How Digital Wallets Work

Digital wallets store payment information, like credit and debit card details, securely on your device. This information is then used to make contactless payments in stores or online. Near-field communication (NFC) technology allows for tap-to-pay transactions at physical terminals.

When you make a purchase, the digital wallet transmits the necessary payment data to the merchant’s point-of-sale system. This process bypasses the need to physically swipe or insert your card. Tokenization replaces sensitive card numbers with unique tokens, adding an extra layer of security.

What Digital Banks Offer

Digital banks primarily offer banking services accessible entirely online. They typically provide standard features like checking and savings accounts, money transfers, and bill pay.

Many also offer debit and credit cards, along with additional features such as budgeting tools, early direct deposit, and virtual card numbers for added security.

A key differentiator is often lower fees compared to traditional banks. Many digital banks do not charge monthly maintenance fees, overdraft fees, or ATM fees. Some even offer interest-bearing checking accounts or higher-than-average interest rates on savings accounts.

Licensing and Regulation Comparison

A key distinction between digital wallets and digital banks lies in their licensing and regulatory oversight. Digital banks, offering full-scale banking services, operate under traditional banking licenses and are subject to stringent regulations similar to brick-and-mortar banks. This involves rigorous capital requirements, compliance with anti-money laundering (AML) and know-your-customer (KYC) regulations, and periodic audits.

Digital wallets, however, face a lighter regulatory burden. Their licensing requirements vary depending on the services offered and the jurisdiction. While some offering limited functionalities might operate under simpler money transmitter licenses, others offering more advanced features may face increasing regulatory scrutiny as they encroach on traditional banking territory. Understanding these differences is crucial when assessing the security and stability of each platform.

Where They Overlap and Differ

Digital wallets and digital banks often appear similar, leading to confusion. Both exist in the digital realm and offer financial services. The key overlap lies in payment facilitation. Both frequently allow users to make online and in-person purchases.

However, their core functionalities differ significantly. Digital wallets primarily focus on payment processing and transaction management, often linking to existing bank accounts or cards. They prioritize speed and convenience for everyday spending. In contrast, digital banks offer a wider range of banking services, such as account management, savings accounts, loans, and investment options, functioning as a complete banking replacement.

Spending and Saving Capabilities

A key differentiator between digital wallets and digital banks lies in their spending and saving functionalities. Digital wallets primarily focus on payment convenience. They facilitate transactions using linked cards or stored funds, enabling contactless payments, online purchases, and peer-to-peer transfers. While some may offer limited savings features like cashback or rewards programs, their core purpose is spending.

Conversely, digital banks offer a broader range of financial services, encompassing both spending and saving. Like digital wallets, they allow for digital transactions. However, they extend further by providing traditional banking features such as interest-bearing accounts, savings goals, and sometimes even investment options. This makes them a more comprehensive financial management tool.

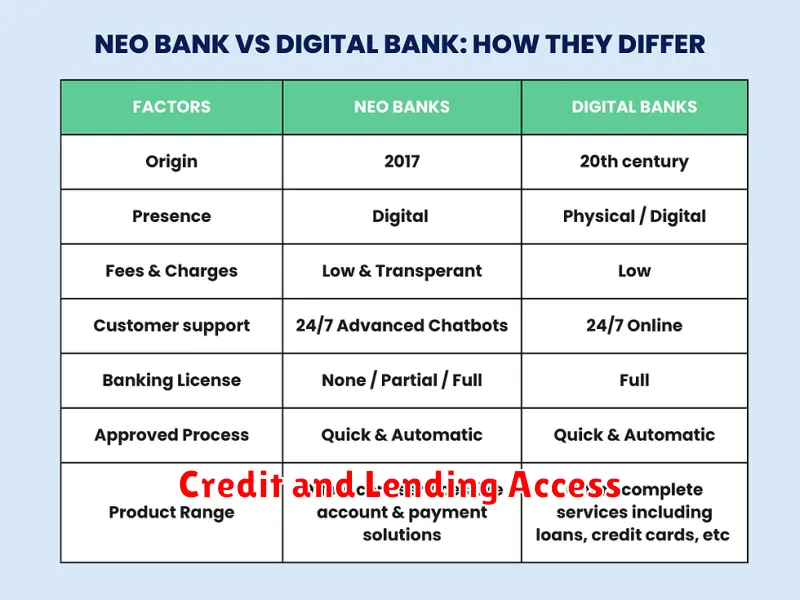

Credit and Lending Access

A key differentiator between digital wallets and digital banks often lies in their credit and lending offerings. Digital wallets primarily focus on payment processing and may offer limited credit options, such as branded prepaid cards or buy-now-pay-later schemes. They generally do not provide traditional lending products like personal loans or mortgages.

Conversely, digital banks, being fully licensed financial institutions, frequently offer a broader suite of credit products. These can include credit cards, overdraft facilities, personal loans, and even mortgages. This distinction arises from the regulatory framework governing each type of institution, with digital banks having greater capacity and authorization to engage in lending activities.

Security and Fraud Prevention

Both digital wallets and digital banks employ robust security measures to protect user funds and data. Multi-factor authentication, encryption, and biometric logins are common features.

Digital wallets often benefit from tokenization, where virtual card numbers replace actual card details during transactions, minimizing risk if compromised. Digital banks typically adhere to strict regulatory guidelines and utilize advanced fraud detection systems.

However, user vigilance remains essential. Strong passwords, regularly monitoring transactions, and being wary of phishing attempts are crucial for both platforms. While both offer considerable security, understanding their specific features and limitations is vital for informed financial management.

Ideal Use Cases for Each

Digital wallets excel for contactless payments in physical stores and online. They are also useful for storing loyalty cards, tickets, and other digital passes. Their strength lies in the convenience and speed they offer for everyday transactions.

Digital banks shine when it comes to managing core banking needs. This includes holding deposits, transferring funds, paying bills, and accessing other financial products like loans or investment accounts. Their focus is on providing comprehensive financial services, often at lower costs than traditional banks.

Which Is Best for You?

Choosing between a digital wallet and a digital bank depends on your financial needs. If your priority is convenient spending and money transfers, a digital wallet might be sufficient. Think about how frequently you use contactless payments or send money to friends and family.

However, if you’re looking for a more comprehensive financial solution that includes features like saving, budgeting, and investing, then a digital bank may be a better fit. Consider whether you need access to traditional banking services like a debit card, bill pay, and direct deposit.

Ultimately, the best choice is the one that aligns with your individual financial goals. You might even find that using both a digital wallet and a digital bank offers the most flexibility and convenience.

{kind=link}