API banking is rapidly transforming the landscape of digital finance. It plays a crucial role in fostering innovation, driving competition, and enhancing the customer experience. By enabling seamless integration between financial institutions and third-party providers, APIs unlock new possibilities for delivering financial services. This introduction will explore the vital role of API banking in shaping the future of digital finance, focusing on its key features, benefits, and impact on the industry. Understanding the power of APIs is essential for anyone involved in the evolving world of fintech and financial services.

From enabling real-time payments and personalized financial management tools to facilitating the growth of open banking, API banking has become indispensable. This article will delve into the specifics of how APIs are empowering both businesses and consumers within the digital finance ecosystem. We will examine the impact of API banking on areas such as payments, lending, and wealth management, while also considering the security and regulatory implications of this transformative technology. By understanding the mechanics and potential of API banking, you will be better equipped to navigate the complexities of modern digital finance.

What Is API Banking?

API banking refers to the practice of using Application Programming Interfaces (APIs) to enable third-party developers to access and integrate banking data and services into their own applications and platforms.

These APIs act as messengers, allowing different software systems to communicate and exchange information securely and efficiently. This opens up a wide range of possibilities for creating innovative financial products and services.

Essentially, API banking allows external applications to connect with a bank’s core systems, enabling seamless data sharing and transaction processing.

How APIs Enable Digital Innovation

Application Programming Interfaces (APIs) are the backbone of modern digital innovation. They act as digital bridges, allowing different software systems to communicate and exchange data seamlessly.

This interoperability fosters a collaborative ecosystem where businesses can leverage each other’s strengths. For example, a ride-sharing app can integrate with a mapping service via API, providing real-time location data without building its own mapping technology. This reduces development costs and accelerates time to market.

APIs also unlock new revenue streams by enabling businesses to share their data and functionalities with third-party developers. This creates a network effect, expanding the reach and potential of individual services while driving innovation across entire industries.

Open Banking and Interoperability

Open banking, facilitated by APIs, fosters greater interoperability within the financial ecosystem. This allows authorized third-party providers to access customer financial data and offer innovative services.

This increased connectivity leads to enhanced competition, driving the development of better products and services. Customers benefit from personalized financial management tools, tailored offers, and streamlined processes. For example, account aggregation apps can provide a holistic view of a customer’s finances across multiple institutions.

Standardization of APIs is critical for seamless integration and secure data exchange. Common API frameworks ensure consistent functionality and reduce the complexity of connecting different platforms.

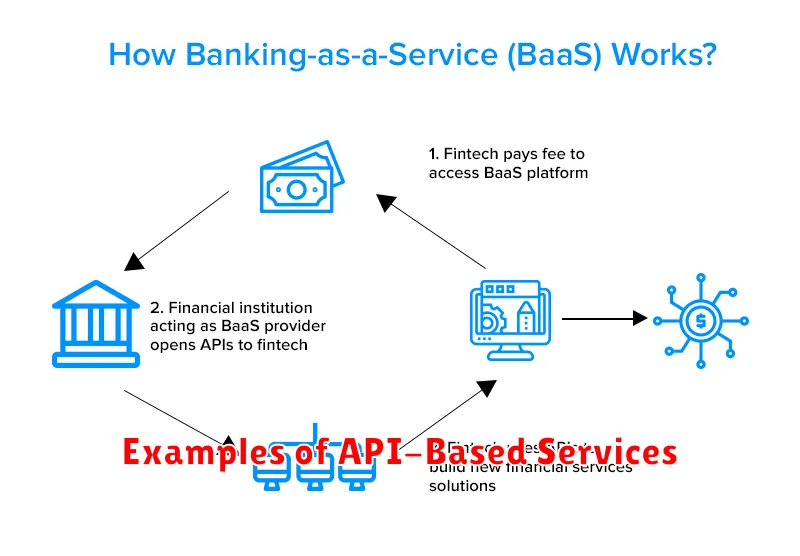

Examples of API-Based Services

API banking facilitates a wide range of services within the digital finance ecosystem. Account Information Services allow authorized third-party providers to access account balances and transaction history. This empowers users with aggregated financial views and personalized budgeting tools.

Payment Initiation Services enable users to initiate payments directly from their bank accounts through third-party applications, streamlining online purchases and bill payments. Fund Transfer Services similarly leverage APIs to move money between accounts quickly and efficiently.

Beyond these core functionalities, APIs also support services like KYC/AML verification, credit scoring, and personalized financial advice, further enriching the digital finance landscape.

Customizing User Experiences

API banking empowers financial institutions to create highly customized user experiences. By opening up their systems, banks can allow third-party developers to build applications tailored to specific customer needs.

This level of personalization extends beyond basic banking functions. Think of budgeting apps that connect directly to bank accounts, investment platforms integrated with spending habits, or customized financial advice delivered through a user’s preferred communication channels.

The result is a more engaging and intuitive financial experience for the user, fostering increased satisfaction and loyalty.

Banking as a Platform (BaaP)

Banking as a Platform (BaaP) represents a significant evolution in financial services. It allows third-party developers to build applications and services on top of a bank’s existing infrastructure through APIs. This transforms the bank from solely a provider of financial products to a platform facilitator.

BaaP fosters innovation and competition by creating an open ecosystem. It allows fintech companies and other businesses to offer customized financial solutions, integrating banking services seamlessly into their offerings. This, in turn, provides customers with a wider range of choices and a more integrated financial experience.

Key benefits of BaaP include increased reach for banks, faster product development, and enhanced customer engagement.

Regulations Around API Usage

API usage in banking is subject to various regulations designed to protect consumer data and maintain financial system stability. These regulations often vary by jurisdiction and are constantly evolving to adapt to the rapid pace of technological advancement.

Key areas of focus include data privacy, security, and consumer consent. Regulations like GDPR and CCPA influence how personal data is handled via APIs. Strong authentication and authorization mechanisms are crucial for secure API access.

Financial institutions must comply with existing regulations like PSD2 in Europe, which mandates open banking and establishes guidelines for third-party access to customer data. Furthermore, regulators are actively working to establish clear frameworks for API usage in finance, addressing issues such as liability and operational resilience.

Security Considerations with APIs

API security is paramount in the context of digital finance. Open banking, driven by APIs, exposes sensitive financial data, making robust security measures crucial.

Key considerations include authentication and authorization. Strong authentication mechanisms are necessary to verify the identity of parties accessing the API. Equally important is authorization, which ensures that only permitted actions are performed on the data.

Data encryption, both in transit and at rest, is essential to protect sensitive information from unauthorized access. Regular security audits and penetration testing are crucial to identify and address vulnerabilities.

Benefits for Developers and Users

API banking offers numerous advantages for both developers and end-users. For developers, it allows for rapid integration of financial services into their applications. This reduces development time and costs, allowing them to focus on core product features. Increased flexibility and customization are also key benefits, enabling developers to tailor financial functionalities to specific user needs.

Users benefit from a seamless and integrated experience. Access to a wider range of financial services within their preferred applications streamlines financial management. Enhanced security measures provided by API banking contribute to a safer online experience. Improved transparency and control over financial data further empowers users to make informed decisions.

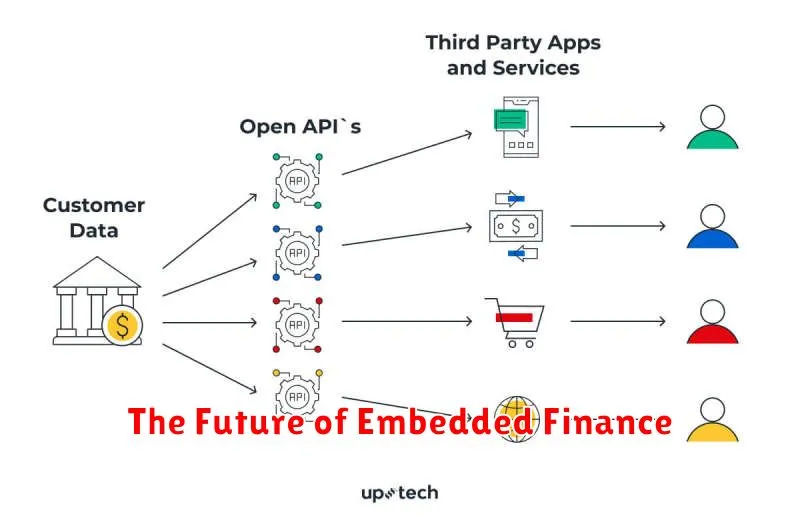

The Future of Embedded Finance

Embedded finance is poised for significant growth. Its seamless integration of financial services into non-financial platforms is transforming how businesses and consumers interact with money. This evolution is driven by increasing demand for frictionless financial experiences.

Key future trends include the expansion into new sectors like healthcare and education. We also anticipate more personalized financial solutions powered by advanced data analytics and AI. Furthermore, the increasing convergence of embedded finance with other emerging technologies, like the Internet of Things (IoT), will create entirely new possibilities.

Regulation will play a crucial role in shaping this future, addressing data privacy and security concerns while fostering innovation.

{kind=link}