The financial landscape is rapidly evolving, and at the forefront of this transformation are neobanks. These digital-first banking institutions are challenging traditional banking models, offering innovative services and attracting a growing number of customers. Understanding the rise of neobanks is crucial for anyone interested in the future of finance, whether you’re a seasoned investor, a tech enthusiast, or simply curious about how you manage your money. This article will delve into the key aspects of neobanks, exploring their features, benefits, and potential impact on the banking industry.

From streamlined mobile banking experiences to personalized financial management tools, neobanks are redefining what it means to bank in the digital age. We’ll explore what sets neobanks apart from traditional banks, examining their advantages and disadvantages, and discussing the regulatory landscape that shapes their operations. This comprehensive overview will provide you with the essential knowledge you need to navigate the world of neobanks and make informed decisions about your financial future.

What Are Neobanks?

Neobanks are digital-only banks, meaning they operate exclusively online without traditional physical branches. They offer many of the same services as traditional banks, such as checking and savings accounts, money transfers, and debit cards.

Neobanks often distinguish themselves through lower fees, user-friendly mobile apps, and specialized features catering to specific demographics or financial needs.

While some neobanks have their own banking licenses, others partner with established banks to provide their services.

How Neobanks Differ from Traditional Banks

Neobanks distinguish themselves from traditional banks primarily through their digital-first approach and lack of physical branches. They operate exclusively online, offering services through websites and mobile apps.

Cost structures also differ significantly. Neobanks typically have lower overhead costs, allowing them to offer higher interest rates on savings accounts and charge lower fees. Traditional banks, burdened by the costs of maintaining physical branches, often have less competitive rates and higher fees.

While traditional banks offer a full suite of financial services, including loans and investment products, some neobanks focus on a niche market, such as providing banking services for freelancers or small businesses.

Key Services Offered by Neobanks

Neobanks distinguish themselves by offering a range of convenient and often cost-effective financial services, primarily through digital platforms. These services often include account opening and management, allowing users to quickly set up and control their finances.

Money transfers are usually a core feature, often facilitating both domestic and international transactions. Debit and prepaid cards are commonly provided, enabling spending and ATM access. Many neobanks also offer budgeting and financial management tools within their apps to help users track their spending and savings.

Some neobanks have expanded to provide additional services such as lending and investment options, broadening their appeal to a wider range of customers.

Popular Neobank Features

Neobanks distinguish themselves through a range of innovative features designed to enhance the banking experience. Account aggregation allows users to view all their financial accounts in one place, simplifying money management. Spending analysis tools provide insights into spending habits, budgeting, and financial goals.

Real-time transaction notifications offer immediate alerts for any account activity, enhancing security and awareness. Many neobanks also offer virtual and physical cards, providing flexibility for various payment scenarios. Some neobanks also offer early paycheck access and savings features such as automated savings plans or high-yield savings accounts.

International money transfers are often streamlined and more affordable through neobanks, benefiting global citizens. Additionally, many neobanks boast 24/7 customer support accessible through various channels like in-app chat or email.

Regulation and Licensing Differences

A key distinction between traditional banks and neobanks lies in their regulatory landscape. Traditional banks operate under established banking licenses and are subject to stringent regulatory oversight by central banking authorities. This framework ensures financial stability and consumer protection.

Neobanks, however, navigate a more diverse regulatory environment. Some operate under full banking licenses, mirroring traditional banks. Others partner with established banks to leverage their existing licenses. A third approach involves operating under specialized licenses, focusing on specific financial services like money transfers or lending, often with lighter regulatory requirements compared to full-fledged banking licenses.

This difference in licensing can impact the level of consumer protection and the range of services offered. Understanding the specific licensing model of a neobank is crucial for informed decision-making.

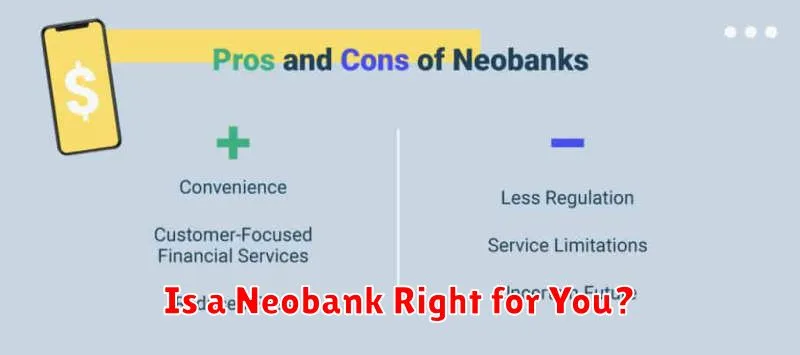

Benefits: Speed, Simplicity, and Savings

Neobanks offer several key advantages over traditional banking. Speed is a primary benefit. Account opening often takes minutes, not days. Transactions are typically processed faster, and customer support is frequently more responsive.

Simplicity is another defining feature. Neobanks boast user-friendly mobile apps designed for intuitive navigation and easy account management. They often eliminate complex paperwork and unnecessary fees.

Savings are a significant draw for many customers. Neobanks often offer higher interest rates on savings accounts and lower fees compared to traditional banks. This can translate to more money in your pocket.

Limitations and Potential Risks

While neobanks offer numerous advantages, it’s crucial to acknowledge their limitations and potential risks. One key area of concern is limited product offerings. Some neobanks may not provide all the services of traditional banks, such as mortgages or loans.

Financial stability is another important consideration. As newer institutions, their long-term viability may be less certain than established banks. Customers should be aware of deposit insurance and regulatory oversight in their region.

Technological dependence presents both advantages and risks. System outages or cybersecurity breaches could disrupt access to funds and services.

Customer Support Models

Neobanks typically employ a variety of customer support models, often prioritizing digital channels. Chatbots and in-app messaging are frequently used for immediate support and answering common questions. This allows for 24/7 availability and quick response times.

For more complex issues, neobanks may offer email support or phone support, though availability can vary. Some neobanks also utilize social media platforms as a channel for customer interaction and support.

Adoption Trends Around the World

Neobank adoption rates vary significantly across the globe. Factors driving this variation include existing financial infrastructure, regulatory landscapes, and consumer tech savviness.

Regions with high mobile penetration and a younger demographic, such as parts of Asia, Latin America, and Africa, have seen rapid neobank growth. These areas often have underserved populations seeking accessible and affordable financial services.

In contrast, established markets like North America and Europe, while experiencing growth, demonstrate a more gradual adoption curve. Consumers in these regions often have existing relationships with traditional banks and are less likely to switch entirely.

Is a Neobank Right for You?

Deciding if a neobank fits your needs depends on your financial priorities. Neobanks excel in specific areas, making them attractive to certain demographics.

Tech-savvy individuals who prefer managing finances entirely through digital platforms will appreciate the streamlined interfaces and advanced features. Those seeking lower fees, especially for international transactions or ATM withdrawals, might find neobanks advantageous.

However, if you require in-person banking services or prefer a more traditional banking relationship, a neobank might not be the best fit. Consider your banking habits and needs when making your decision.

{kind=link}